Choosing a High Risk Merchant Account: A Complete Guide

How to Choose a High Risk Merchant Account

You’ve launched your site, sales are booming, and then you receive a devastating email: your payment processor has frozen your funds. According to industry data, standard payment aggregators can lock your money away for 60 to 90 days without warning.

Being labeled "high risk" feels like a harsh accusation. In reality, this is just a standard banking category, not a moral judgment on your business. Selling supplements or coaching services isn't shady, but it does require a specialized financial toolkit because mainstream platforms aren't built for your specific industry nuances.

Understanding the critical differences of a payment aggregator vs dedicated merchant account is your path to stability. Choosing the right high risk merchant account gives you a true partner who protects your predictable cash flow instead of panicking over chargebacks.

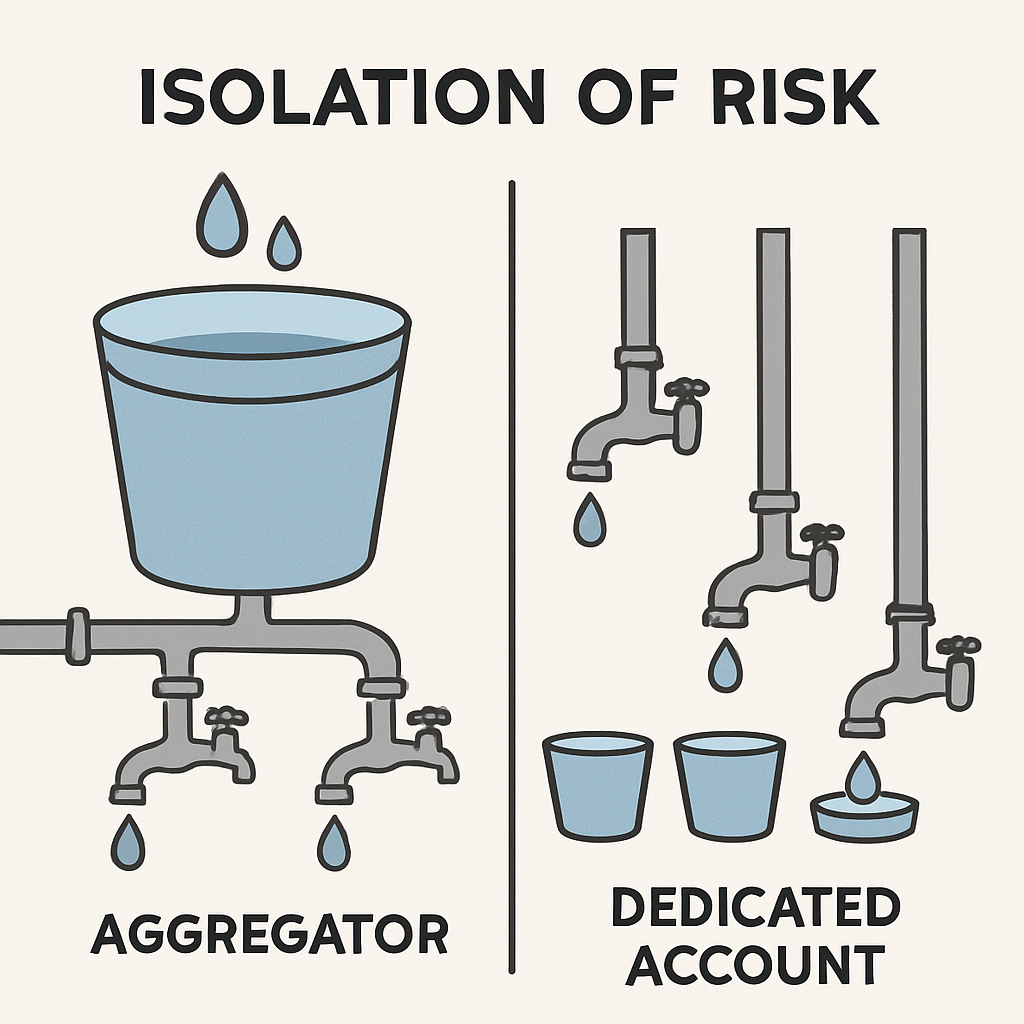

Aggregators vs. Dedicated Accounts: Why Your 'Easy' Setup is a Ticking Clock

Signing up for standard payment platforms feels magical due to "back-end underwriting," a process where companies let you accept credit cards instantly and audit your business later. For supplement brands or online coaches, that delayed review is exactly when sudden fund freezes happen.

These aggregators rely on "risk pooling" by mixing your transactions with thousands of others in one massive bucket. When analyzing a high risk merchant account vs low risk setups, remember this shared pool makes your store vulnerable to other businesses' chargebacks and mistakes.

A dedicated account solves this vulnerability through "front-end underwriting," meaning the bank thoroughly approves your specific business before you process a single dime. Though high risk credit card processing fees can sometimes vary here, this upfront verification provides isolated financial plumbing and ensures absolute cash flow stability.

Since this initial approval is the ultimate safety net for your revenue, preparation is everything.

Passing the Underwriting 'Job Interview': What High-Risk Banks Really Want to See

Treating your application like a professional interview is key to surviving the mandatory underwriting requirements for high risk businesses. Banks perform KYC (Know Your Customer)—a strict background check verifying your business identity—to ensure you are financially stable and fully transparent about what you sell.

To speed up approval, prepare a "loan-ready" package. Your high risk merchant account application checklist must include these six items:

- 3 months of business bank statements

- A utility bill verifying your address

- Your official business license

- Your SSN and EIN

- Previous processing history

- Marketing materials

Beyond paperwork, underwriters scrutinize your digital footprint to assign your Merchant Category Code (MCC), a four-digit number classifying your exact industry. The impact of merchant category codes on processing is massive, as this single number dictates your baseline fees and overall risk tier. Furthermore, if your website lacks an "About Us" page or hides its refund policy, banks will assume you generate high customer complaints, instantly damaging your risk score.

Securing this initial approval gets your foot in the door with a reliable banking partner. From there, you must navigate the financial realities of that partnership, including risk management and processing costs.

The High Cost of Risk: Understanding Rolling Reserves and Hidden Processing Fees

Securing approval is a relief, but you must understand how processors manage financial exposure before signing a contract.

Navigating hidden costs in high risk merchant services requires mastering your fee structures and account holds. Carefully compare these common models:

- Tiered vs. Interchange-plus: Avoid tiered pricing, which uses misleading "teaser rates" to overcharge you later. Demand Interchange-plus, a transparent model passing the direct bank wholesale cost to you plus a fixed, predictable markup.

- High risk merchant account reserve types: A Rolling Reserve acts as a security deposit, holding a portion of daily sales (e.g., 10%) for six months to cover potential refunds. A Capped Reserve retains a percentage until reaching a set dollar target, and an Up-front Reserve requires an initial cash deposit.

Factoring these required holds into your profit margins ensures you can still consistently pay your suppliers. Furthermore, avoiding high risk merchant account scams means strictly challenging fabricated "junk fees," such as unexplained monthly minimums.

Fortunately, restrictive banking terms are rarely permanent. By proving your reliability, you can negotiate better conditions, though maintaining those terms requires actively managing red flags to keep your account active.

Reducing the Red Flags: How to Lower Your Chargeback Rates and Keep Your Account

Imagine having your processing shut off entirely because a few customers simply forgot what they bought. That is the danger of ignoring your Chargeback Ratio, which is the percentage of sales customers forcibly reverse through their bank rather than asking you for a standard refund.

Defending your revenue requires evaluating the top rated high risk payment gateways. Think of a Payment Gateway as a digital cashier—software that securely transmits card data and blocks fraudulent orders. If your ratio still runs high despite this software, comparing offshore vs domestic high risk processing becomes necessary, as international banks tolerate higher dispute volumes.

Learning how to reduce high risk chargeback rates relies on these four essential tactics:

- Clear Descriptors: Make sure your billing name—the Descriptor on a customer's bank statement—matches your brand exactly.

- 24/7 Support: Give buyers an immediate contact option.

- Alert Services: Use third-party tools that warn you before disputes become official.

- Mandatory Checkboxes: Require policy agreement before checkout.

Mastering these protective steps proves your reliability to underwriters and sets a foundation for sustainable processing.

Your 3-Step Plan to Secure a Stable High-Risk Merchant Account

Transitioning from frustrating rejections to true financial stability is entirely within your control. A dedicated merchant account is a vital investment in your business longevity, not just another processing cost.

Start your transition timeline today by auditing your current risk and gathering your underwriting documents. Prioritize matching high risk processors to your business type instead of simply hunting for the lowest rate. Ensure your chosen partner also provides hands-on support for maintaining PCI compliance for high risk merchants.

Once your account is live, establish a monthly risk health check to review chargebacks and spot potential red flags early. This structured approach protects your cash flow and keeps your business thriving.